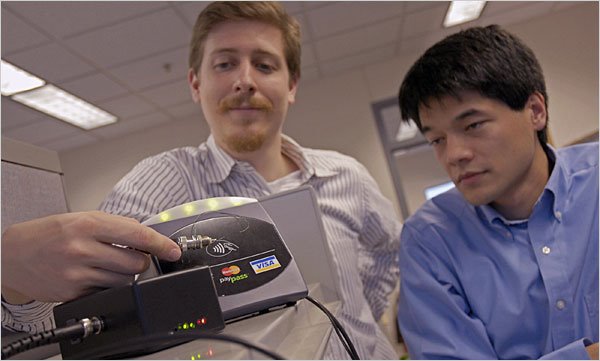

Marilyn Surfus realized last weekend that she’d forgotten her checkbook at home. But the slip didn’t stop her from buying groceries. She simply placed her finger on the scanner pad in the checkout lane at Scott’s Food & Pharmacy. The device compared hundreds of pre-selected points on her fingerprint for comparison with her data already on file. And the sale was approved.

Marilyn Surfus realized last weekend that she’d forgotten her checkbook at home. But the slip didn’t stop her from buying groceries. She simply placed her finger on the scanner pad in the checkout lane at Scott’s Food & Pharmacy. The device compared hundreds of pre-selected points on her fingerprint for comparison with her data already on file. And the sale was approved.Scott’s is piloting the Pay by Touch system at four of its Fort Wayne stores: the Dupont, Coventry, Georgetown and Stellhorn locations. Rick Zahm, Scott’s vice president of merchandising and operations, said the first units were installed last week. Company officials plan to install the devices in the chain’s 14 remaining northeast Indiana stores in about two weeks.

Krista Thomas, Pay by Touch

spokeswoman, said Scott’s is the first company in northeast Indiana to adopt the high-tech payment system. Touch payments are accepted in 2,400 retail outlets in 44 states; 3.3 million people have enrolled in the system, Thomas said.

spokeswoman, said Scott’s is the first company in northeast Indiana to adopt the high-tech payment system. Touch payments are accepted in 2,400 retail outlets in 44 states; 3.3 million people have enrolled in the system, Thomas said.The technology allows consumers to enroll at a bright green kiosk near the front office. That process – which involves presenting a driver’s license, a voided check and making that initial finger scan – is all done electronically and takes about three or four minutes.

Afterward, the customer can simply touch the scanner at a checkout to have a purchase covered with money withdrawn from the customer’s checking account. The technology also allows for payments with debit and credit cards but, so far, Scott’s has opted to offer only Automatic Clearing House withdrawals from checking accounts. Such transactions have lower fees for merchants than debit purchases. Either way, the money is taken from the customer’s checking account.

After a person has enrolled in the system, he can use it to pay for purchases at any retailer that offers the option. Thomas said participating businesses include gas stations, convenience stores, banks and check-cashing companies.

Scott’s processed about 40 Pay by Touch transactions last weekend, including the one by Surfus, the company’s supervisor of bookkeeping and customer service. She previously enrolled in the system while visiting another grocery in Chicago. Scott’s has concentrated on signing up employees so that they can become familiar with the system and more easily explain it to curious customers.

Zahm, the Scott’s vice president, describes the system as the wave of the future – but one that will be quickly embraced in the present by customers who like to get in and out of stores quickly. “We can tell it’s going to be successful, based on signups,” Zahm said.

He declined to give exact numbers for competitive reasons. He also declined to put a dollar amount on installing the technology. Zahm said, however, that Pay by Touch shared the cost with the company.

Lindsay Hancock, spokeswoman for The Fresh Market, said the Greensboro, N.C.-based chain hasn’t adopted the technology and isn’t considering it, as far as she knows. Some consumers have been reluctant to embrace the high-tech process. Thomas, of San Francisco-based Pay by Touch, acknowledged that some people are hesitant to register because they don’t want their fingers scanned. But soon, even they realize how safe the transaction is compared to writing checks or using debit cards.

“There’s usually an initial concern about security and privacy,” she said. “And we respond that we have the most robust security that can exist.” (see Contactless Cards Provide Contacts and Numbers) to read about real flaws in privacy)

The company works with IBM and doesn’t store any of the data at retail locations. In fact, the cashier doesn’t even see the customer’s checking account number, adding a layer of security, Thomas said.

Pay by Touch has talked to participants and found that older adult women appreciate not having to carry their purses, which could be lost or stolen, Thomas said.

{kind=link}

{kind=link}